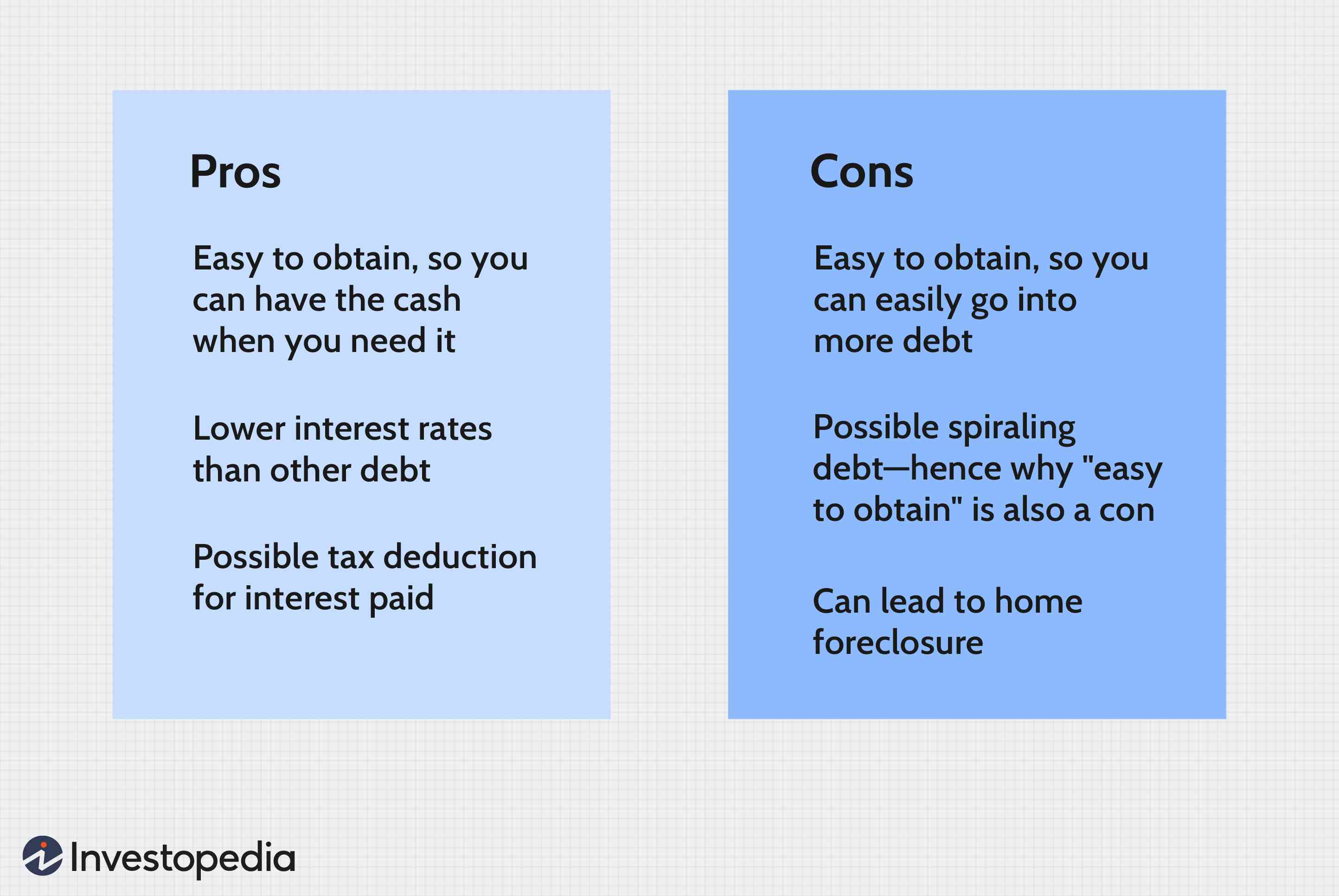

A reverse mortgage is a loan that allows you to borrow against the equity in your home. Your equity refers to the difference between the home's value and the mortgage balance. As your home becomes more valuable, your equity will also increase. The lowest-cost type of reverse mortgage is the Single-Purpose reverse mortgage. These loans are easy to qualify for and the interest rates are very low.

Private reverse mortgages are not subject to strict eligibility requirements

Reverse mortgages that convert to home equity are the most common. These mortgages are covered by the Federal Housing Administration, and have strict eligibility requirements. To be eligible for HECMs, homeowners must have a mortgage balance less than $150,000 and be at least 60 years old. HECMs may be availed as monthly or lump-sum payments.

Reverse mortgage borrowers do not have to make monthly mortgage payments, but they must still pay regular housing costs. These expenses may include homeowners insurance premiums as well as property taxes. Reverse mortgage agreements usually require that borrowers maintain current status with property taxes. The lender may require repayment of the remainder if the borrower fails to pay the required fees.

One-purpose reverse mortgages are among the most affordable of the three options.

The most cost-effective option is single-purpose mortgages. They are not accessible everywhere. Typically, they are only available through state and local governments, nonprofit organizations, and some credit unions. Do your research to find a good lender. Compare the information that you get from each lender and avoid high-pressure sales tactics or hidden fees.

Reverse mortgages can be used for one purpose and are available in different terms. Unlike other types of reverse mortgages, they do not require monthly repayments. These loans will become due if the borrower stops paying homeowners' insurance or if the municipality condemns the property. Your age and your home's value will determine how much you can borrow. Additionally, you have the option to opt for the term option. This allows cash advances to be made monthly for a certain period.

Interest rates

Lenders may have different interest rates for reverse mortgages. Some lenders offer fixed rate mortgages while others offer variable rates. Fixed rate reverse mortgages will give you a higher initial payout than variable rate ones, but their rates may change over time. The average interest rate for a HECM is 5.060%, according to the National Reverse Mortgage Lenders Association. Variable rate reverse mortgages are subject to market fluctuations. You should consult your lender for current rates.

A variable rate reverse mortgage will fluctuate based on external factors, so the rate you pay can be different in each year. This is a great option if you plan to only use the funds occasionally. This type of loan also offers protection against rate hikes as it can only rise by 2% every year. The maximum interest rate increase over the life of the loan is typically 5%.

Reverse mortgages can help you get your money back

Reverse mortgages are available to people in retirement who need to access a lump sum of money. These loans can be combined with a credit line, which allows the borrower access to the full amount at once. These loans can be more expensive than either monthly payments or line-of credit options. The loans are also more risky, especially for younger borrowers.

People who are currently in the process to get a mortgage reverse should be wary if a salesperson tries to rush them. These salespeople might push you to sign a contract and/or take a lumpsum payment. It is best to research the reverse mortgage counselor that you feel most comfortable with.

FAQ

Is it better for me to rent or buy?

Renting is typically cheaper than buying your home. However, you should understand that rent is more affordable than buying a house. The benefits of buying a house are not only obvious but also numerous. For example, you have more control over how your life is run.

Should I use a mortgage broker?

A mortgage broker may be able to help you get a lower rate. Brokers can negotiate deals for you with multiple lenders. Some brokers receive a commission from lenders. Before signing up, you should verify all fees associated with the broker.

How can I calculate my interest rate

Market conditions can affect how interest rates change each day. The average interest rate during the last week was 4.39%. Add the number of years that you plan to finance to get your interest rates. For example: If you finance $200,000 over 20 year at 5% per annum, your interest rates are 0.05 x 20% 1% which equals ten base points.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

External Links

How To

How to purchase a mobile home

Mobile homes can be described as houses on wheels that are towed behind one or several vehicles. Mobile homes were popularized by soldiers who had lost the home they loved during World War II. People today also choose to live outside the city with mobile homes. These homes are available in many sizes and styles. Some are small, while others are large enough to hold several families. There are some even made just for pets.

There are two types of mobile homes. The first is made in factories, where workers build them one by one. This process takes place before delivery to the customer. A second option is to build your own mobile house. The first thing you need to do is decide on the size of your mobile home and whether or not it should have plumbing, electricity, or a kitchen stove. You will need to make sure you have the right materials for building the house. To build your new home, you will need permits.

Three things are important to remember when purchasing a mobile house. You may prefer a larger floor space as you won't always have access garage. If you are looking to move into your home quickly, you may want to choose a model that has a greater living area. Third, you'll probably want to check the condition of the trailer itself. Problems later could arise if any part of your frame is damaged.

You need to determine your financial capabilities before purchasing a mobile residence. It is crucial to compare prices between various models and manufacturers. Also, look at the condition of the trailers themselves. Although many dealerships offer financing options, interest rates will vary depending on the lender.

It is possible to rent a mobile house instead of buying one. Renting allows for you to test drive the model without having to commit. Renting isn’t cheap. Renters usually pay about $300 per month.