HELOCs have the benefit of being flexible and allowing you to make payments when needed. Payments can be made with a credit card, a check or cash from the bank. The amount of interest you pay is usually not included in your monthly payments. Your draw period payment is small. HELOCs permit you to pay off the principal loan, but you will be charged fees if this happens.

Variations in interest rates are possible over time

HELOCs provide a great opportunity to obtain credit at a low interest rate and for a prolonged period. You should compare interest rates as they can fluctuate over time so you can find the best rate for your needs. Even a slight difference in interest rates can have a huge impact on how much you end-up paying over the term of your loan.

Interest rates on HELOCs are usually variable and are based on a few factors, including the prime rate and the federal funds rate. The prime rate is generally three percentage point higher than the federal fund rate and lenders often base their HELOC interest rates on that.

The draw period for a HELOC ranges from 10 to 20 year. This is the time that the borrower is allowed to withdraw money from the line. The borrower has the right to make the required payments for the balance of the loan until it is fully repaid.

Refinance or shut down a HELOC after the draw period expires

A HELOC is a good financial tool if used correctly. If you don't pay the loan off within the set time, it could become a trap. You can avoid this by reviewing the terms of the loan carefully. HELOCs tend to be variable-rate loans. This means that the interest rates can change depending upon market conditions.

It is crucial to understand when the draw period ends. HELOCs generally have a 20 Year draw period. The repayment period begins once the draw period has ended. While most lenders will allow you to make interest only payments during the draw period (though they might require that you make a minimum payment which includes some principal), others may not.

Second, it is important to understand the terms of the loan before closing. Avoiding a prepayment penalty by refinancing or closing your HELOC before the draw ends is possible. If you're unsure whether to close the account or refinance it, it's a smart idea to speak with a financial professional or lender.

Tips for a successful Heloc Draw Period

A HELOC is an open line of credit that is based on the equity in your home. This line of credit lets you borrow as much money as you want and pay it off in five or 10 years. Although you will need to pay interest for the amount that is borrowed, you can usually repay less than the amount each month.

A HELOC can be used multiple times throughout the draw period. This is especially useful if you have a lot of ongoing expenses or don't know how much money you will need. You might need to spend a lot on remodeling your garage. This may include hiring a contractor to redo the floor and purchasing cabinets. For the garage to be painted, you might also need to hire an artist. A HELOC allows you to borrow exactly the amount you need.

FAQ

What is the maximum number of times I can refinance my mortgage?

It depends on whether you're refinancing with another lender, or using a broker to help you find a mortgage. Refinances are usually allowed once every five years in both cases.

What is a reverse loan?

A reverse mortgage allows you to borrow money from your house without having to sell any of the equity. It works by allowing you to draw down funds from your home equity while still living there. There are two types available: FHA (government-insured) and conventional. With a conventional reverse mortgage, you must repay the amount borrowed plus an origination fee. FHA insurance covers repayments.

What should I look for when choosing a mortgage broker

Mortgage brokers help people who may not be eligible for traditional mortgages. They compare deals from different lenders in order to find the best deal for their clients. Some brokers charge fees for this service. Others provide free services.

How much will it cost to replace windows

Windows replacement can be as expensive as $1,500-$3,000 each. The cost to replace all your windows depends on their size, style and brand.

Is it possible to get a second mortgage?

Yes. But it's wise to talk to a professional before making a decision about whether or not you want one. A second mortgage can be used to consolidate debts or for home improvements.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

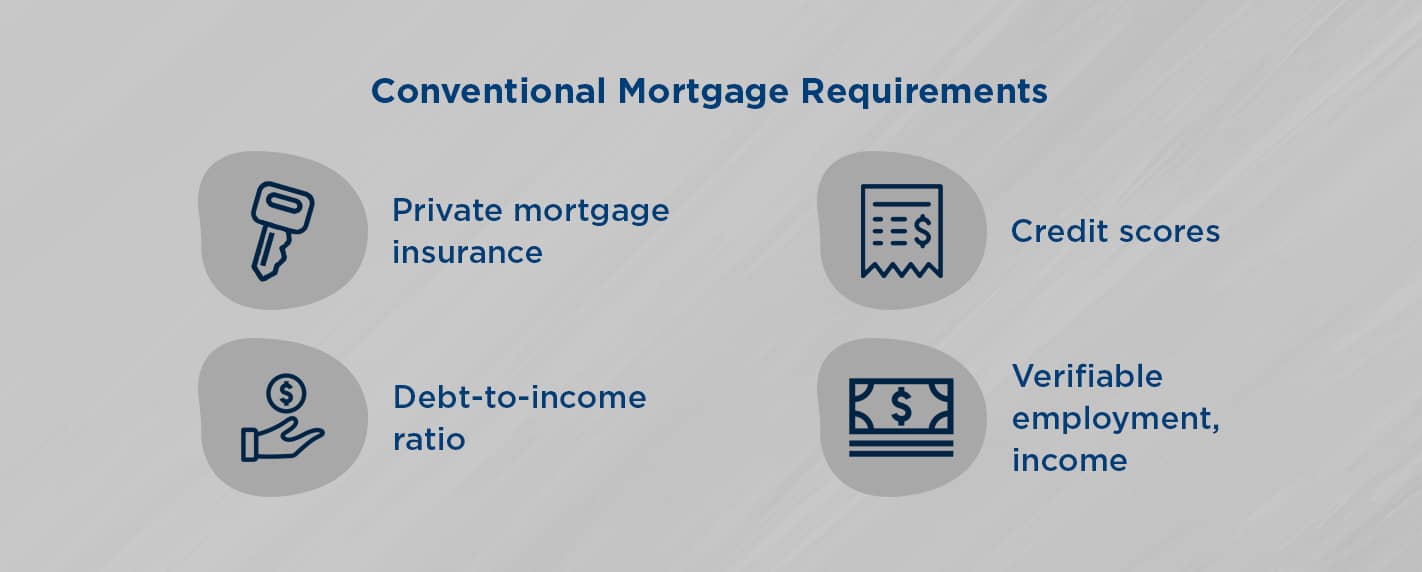

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

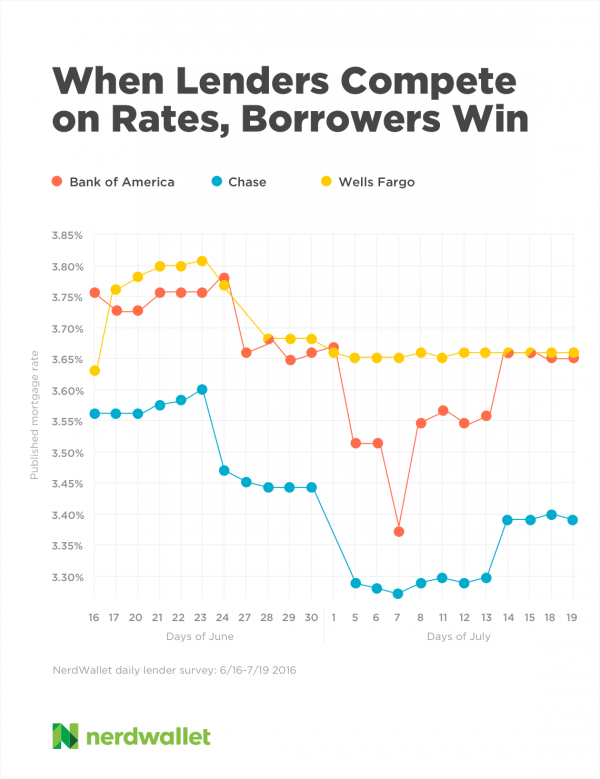

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to buy a mobile house

Mobile homes are houses that are built on wheels and tow behind one or more vehicles. Mobile homes are popular since World War II. They were originally used by soldiers who lost their homes during wartime. Mobile homes are still popular among those who wish to live in a rural area. These houses are available in many sizes. Some houses have small footprints, while others can house multiple families. Even some are small enough to be used for pets!

There are two main types of mobile homes. The first type is produced in factories and assembled by workers piece by piece. This occurs before delivery to customers. You could also make your own mobile home. It is up to you to decide the size and whether or not it will have electricity, plumbing, or a stove. Next, make sure you have all the necessary materials to build your home. Finally, you'll need to get permits to build your new home.

If you plan to purchase a mobile home, there are three things you should keep in mind. First, you may want to choose a model that has a higher floor space because you won't always have access to a garage. Second, if you're planning to move into your house immediately, you might want to consider a model with a larger living area. The trailer's condition is another important consideration. If any part of the frame is damaged, it could cause problems later.

It is important to know your budget before buying a mobile house. It is important that you compare the prices between different manufacturers and models. You should also consider the condition of the trailers. Many dealers offer financing options. However, interest rates vary greatly depending upon the lender.

A mobile home can be rented instead of purchased. You can test drive a particular model by renting it instead of buying one. Renting is not cheap. Most renters pay around $300 per month.