Colorado's current mortgage rates are important to know if you plan on buying a house. These mortgage rates tend to stay relatively stable and seldom fluctuate more than 1% in a six-month period. To find out the current rates in your region, you can visit the websites of real estate and financial institutions. You can also ask your local bank about mortgage rates.

Fixed-rate mortgages

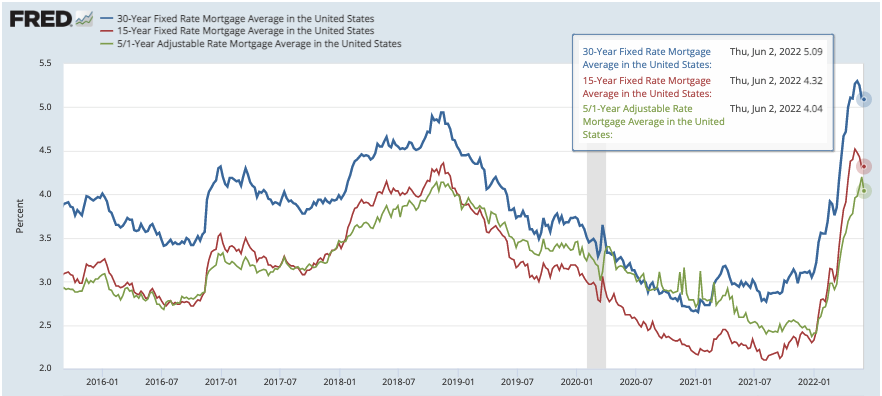

Colorado homeowners who are looking for a home mortgage in Colorado can choose a fixed-rate loan. This loan is guaranteed to have one interest rate for the entire loan term. That means your monthly payment will not change even if the market falls. Fixed-rate mortgages are also more affordable due to their shorter repayment periods. The current average interest rates for a 30-year, fixed-rate mortgage in Colorado are 3.42%.

Colorado offers fixed-rate mortgages with minimum 20% downpayment. These mortgages don't belong to any government program. However, they are good choices for people with good credit. In Colorado, the maximum conforming loan limit is $647,200 for most areas, although it's significantly higher in Denver County and other expensive areas. In Colorado, you must have a credit score at 740 or above to apply for an interest-only loan.

Jumbo loans

Jumbo loans are an option for many Colorado homebuyers who may not be able to qualify conventional mortgages. These loans allow buyers to buy a home at a higher price than the Fannie Mae or Freddie Mac conforming loan limits. These loans typically have slightly higher interest rates.

Jumbo loans are needed for a number of reasons. These loans can be a great way to purchase an expensive home. Contrary to traditional mortgages, there is no requirement for a large down payment. Colorado's majestic Rocky Mountains make it a desirable place for home buyers. There are ranches that offer acres of land for sale, as well modern suburban homes in Denver or Arapahoe County. If you are considering buying a jumbo loan, contact us for a no-obligation quote.

Interest-only loans

There are many different types of mortgage loans available in Colorado, including interest-only mortgages. Fixed interest rates are offered for interest-only mortgages. These loans can be used for a specific number of year. The principal does not decrease during this period, but the monthly payment does. The term of a loan is typically three to five years. It's similar to an ARM loan. After this period, the interest rate will rise, increasing the monthly payment. The buyer must deposit at least 20% to qualify for an interest-only loan. Lenders take into account a variety of factors in determining whether a borrower is eligible for a mortgage.

Interest-only mortgage rates are usually lower than those for jumbo loans. During the early years of a loan, the interest rate can go up a maximum of five percentage points. It cannot increase beyond that point by more than two percentage points. The initial rate will rise if the interest-only period is longer.

Conventional Loans

Colorado Conventional loans can be beneficial to homebuyers who don't have a lot of cash. They usually come with lower fees and are easy to obtain. These grants allow homeowners to rapidly build equity in their homes. They can be used on virtually any property. There are conventional loans available to you, regardless of whether you are buying your first house or intending to sell it over the next few years.

Conventional loans require you to pay between 3% - 20% down payment. This amount can vary from town to town, but in general, you need to invest anywhere from $3,000 to $20,000 to qualify for a conventional loan. These loans are frequently used to finance single-family or investment property, as well second homes.

VA loans

Veterans in Colorado have a number of options when it comes to purchasing a home. The VA loan allows veterans to purchase a home without requiring a down payment. In addition, it doesn't require a monthly mortgage insurance premium. These loans are fairly easy to obtain. Borrowers should only meet the requirements of the lender. Borrowers should speak to at least three lenders before agreeing on one.

The VA loan's mortgage rate is affected by several factors. Comparing loan offers from different lenders will allow borrowers to find the lowest rate and lowest fees. Although it can be tedious, this is the only way you will find the best rate and lowest origination fee.

FAQ

How long does it take for my house to be sold?

It depends on many different factors, including the condition of your home, the number of similar homes currently listed for sale, the overall demand for homes in your area, the local housing market conditions, etc. It can take anywhere from 7 to 90 days, depending on the factors.

How much does it take to replace windows?

Replacement windows can cost anywhere from $1,500 to $3,000. The cost to replace all your windows depends on their size, style and brand.

How can I tell if my house has value?

Your home may not be priced correctly if your asking price is too low. If you have an asking price well below market value, then there may not be enough interest in your home. To learn more about current market conditions, you can download our free Home Value Report.

What should you consider when investing in real estate?

The first thing to do is ensure you have enough money to invest in real estate. If you don’t save enough money, you will have to borrow money at a bank. It is important to avoid getting into debt as you may not be able pay the loan back if you default.

You must also be clear about how much you have to spend on your investment property each monthly. This amount should include mortgage payments, taxes, insurance and maintenance costs.

Also, make sure that you have a safe area to invest in property. You would be better off if you moved to another area while looking at properties.

How long does it take to get a mortgage approved?

It depends on several factors such as credit score, income level, type of loan, etc. It generally takes about 30 days to get your mortgage approved.

Statistics

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to become real estate broker

An introductory course is the first step towards becoming a professional real estate agent. This will teach you everything you need to know about the industry.

Next, you will need to pass a qualifying exam which tests your knowledge about the subject. This involves studying for at least 2 hours per day over a period of 3 months.

This is the last step before you can take your final exam. To become a realty agent, you must score at minimum 80%.

All these exams must be passed before you can become a licensed real estate agent.