When it comes to short sales, the biggest misconception is that it's just about selling the house. The truth is that it's much more complicated than that. The process involves both a borrower and the house. For a successful short-sale transaction, both the buyer and the seller must be understood. Here are some key points to keep your mind on:

Purchase a short sale

A short sale is an excellent way to secure a great price on a house. It requires a bit more effort than buying a traditional house. First, you will need to prove that you cannot make your mortgage payments. You can do so by presenting a hardship notice and proof that you have income. A CMA, which is a compilation of home sales and an estimate of the current value for your house, is another important document.

There are also a few things to look out for when buying a short sale. A short sale home typically has more problems than a normal house. The sellers may not have the money to fix their home. Some sellers are also emotionally distressed and may take their feelings out on the property. A short sale home might be the best option if you aren't interested in major repairs.

Role of the lender in a short-sale

The lender's role in a short-sale is to help a homeowner sell their home for less than the loan balance. A short sale allows a homeowner to pay less than the total loan amount and the bank will take the rest. A short sale can take many months. The lender will not tell the homeowner how much it wants to sell the home for, but will look at what a buyer offers and then decide whether or not to accept it.

If a lender is willing to consider a short-sale request, you can contact the lender's loss mitigation team to submit a short-sale application. Make sure you speak to the same person every time you call. You should explain your situation to the person you are calling and give copies of any supporting documents such as termination letters and medical bills.

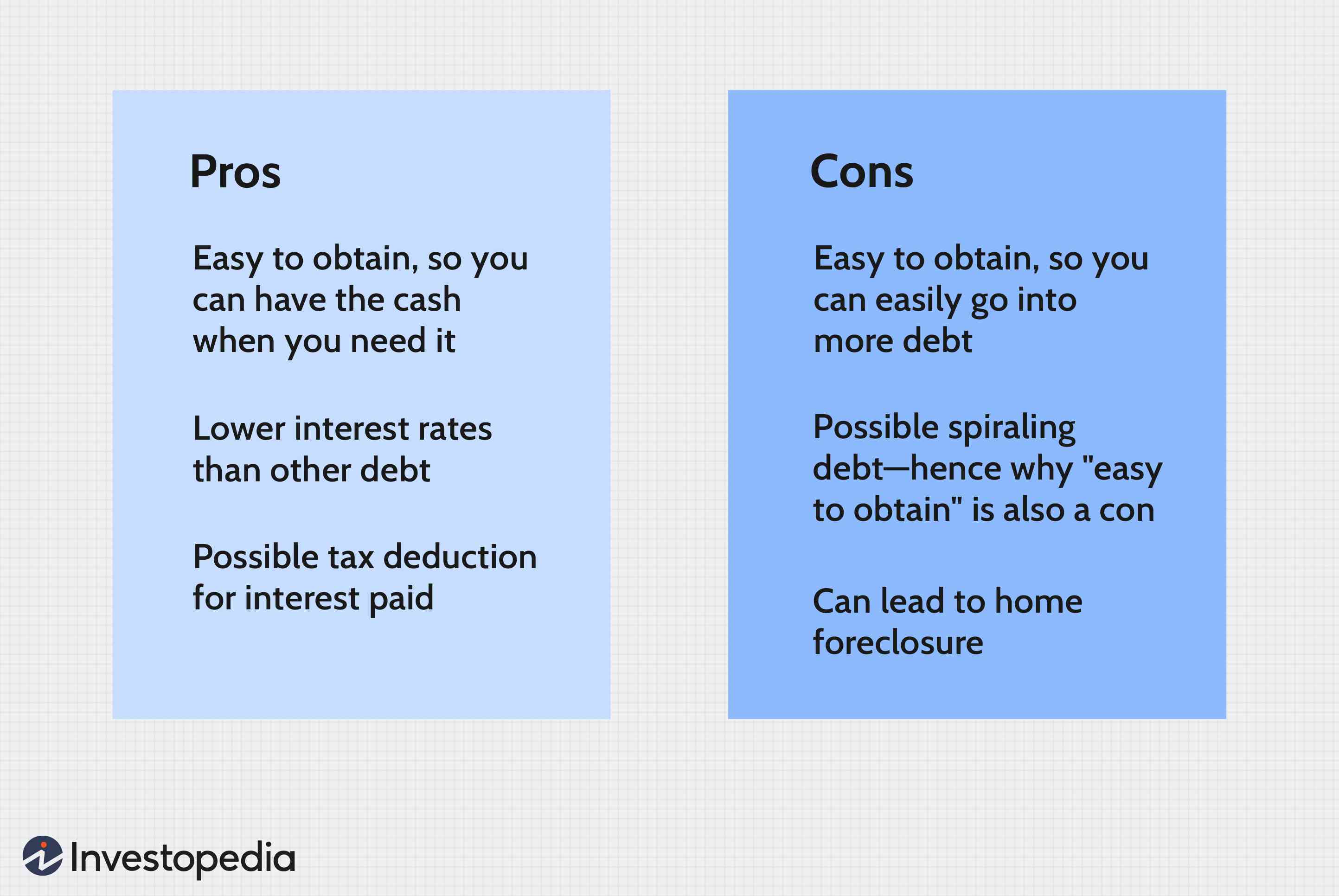

Getting a short sale loan

You may consider getting a loan to finance the purchase of a short-sale home. A short sale loan is different than traditional mortgages. They require a longer approval process. Lenders typically lock in the interest for two months after the sale has been approved. This could mean that depending on the lender you might have to wait several weeks, or even months, to close your loan.

To get a short-term loan, you must first explain your financial situation. To be eligible for a short sale loan, you will need to prove that your ability to pay your mortgage payments is not possible. Your income and debt are usually factors that your lender considers. Your chances of approval are higher if you can reduce your debt significantly.

FAQ

How much money will I get for my home?

The number of days your home has been on market and its condition can have an impact on how much it sells. Zillow.com says that the average selling cost for a US house is $203,000 This

How much money do I need to save before buying a home?

It depends on how much time you intend to stay there. You should start saving now if you plan to stay at least five years. If you plan to move in two years, you don't need to worry as much.

What's the time frame to get a loan approved?

It depends on many factors like credit score, income, type of loan, etc. It generally takes about 30 days to get your mortgage approved.

How much does it cost for windows to be replaced?

Replacing windows costs between $1,500-$3,000 per window. The cost to replace all your windows depends on their size, style and brand.

Should I use a broker to help me with my mortgage?

A mortgage broker may be able to help you get a lower rate. Brokers work with multiple lenders and negotiate deals on your behalf. Some brokers receive a commission from lenders. Before signing up for any broker, it is important to verify the fees.

Which is better, to rent or buy?

Renting is usually cheaper than buying a house. But, it's important to understand that you'll have to pay for additional expenses like utilities, repairs, and maintenance. A home purchase has many advantages. For instance, you will have more control over your living situation.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to find real estate agents

A vital part of the real estate industry is played by real estate agents. They sell homes and properties, provide property management services, and offer legal advice. You will find the best real estate agents with experience, knowledge and communication skills. For recommendations, check out online reviews and talk to friends and family about finding a qualified professional. Consider hiring a local agent who is experienced in your area.

Realtors work with homeowners and property sellers. The job of a realtor is to assist clients in buying or selling their homes. In addition to helping clients find the perfect house, realtors also assist with negotiating contracts, managing inspections, and coordinating closing costs. A majority of realtors charge a commission fee depending on the property's sale price. Unless the transaction closes, however, some realtors charge no fee.

The National Association of REALTORS(r) (NAR) offers several different types of realtors. NAR members must pass a licensing exam and pay fees. The course must be passed and the exam must be passed by certified realtors. NAR designates accredited realtors as professionals who meet specific standards.