While mortgage rates in New York may be higher than in other states, they are still close to historic lows. The current 30-year fixed rate mortgage is at 5.925%. 5.683% for a five-year adjustable mortgage. New York mortgage rates depend on your credit score. You can learn more about the factors that affect your mortgage rate.

Freddie Mac's average mortgage rate is near historic lows

The average mortgage rates at Freddie Mac are close to historic lows. They will likely remain that way for a long time. The 30-year fixed mortgage rate currently stands at 3.26%, which is the second-lowest rate ever recorded by the agency. This week's average mortgage rate is only three basis points lower than the all-time low last week.

The average mortgage rate on 30-year fixed-rate mortgages dropped to 2.80% last week from 2.78% one week ago and 2.99% one year ago. This is a welcome sign for borrowers who have excellent credit with a 20% downpayment and could be the best deal since 2008. However, the average rate of borrowers with lower credit scores and lower down payments could be higher. Rates as low as 6.5% are possible for borrowers with 700 credit ratings. Rates for borrowers are determined by the Fair Isaac Corporation's FICO score.

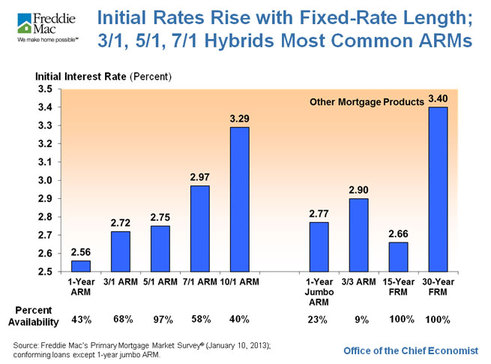

Freddie Mac published a chart that shows the average mortgage rate. These numbers were derived from weekly surveys that the agency collects. These rates have been collected by the agency since 1971 when it was founded. Freddie Mac surveys lenders Mondays through Wednesdays and releases its results Thursday mornings. The survey is based a survey on home purchase mortgages as well as refinances. A 0.5 percent price adjustment is applied to the mortgage amount.

New York's mortgage rates exceed the national average

New York may be a place to look if you are searching for a home loan that has a slightly higher rate of interest. The state's mortgage rates are higher than the average national rate. The 30-year fixed interest rate mortgage in New York starts around 5.68%. While the mortgage with a 15-year term is at 4.73%, it starts at 5.68%. FHA and conventional mortgages are both available in New York. The government-backed mortgages are less expensive for those with bad credit or those who need help paying down their mortgage payments.

There are many factors that affect mortgage rates. The interest rate you receive will be influenced by the state you reside in. The S&P Global Group keeps track on average mortgage rates in each state. Mortgages are secured loans. The lender can use the collateral of your home as security. If you default on your payments, the lender can repossess your home.

Your credit score determines your mortgage rate

Your credit score will play a large role in determining how much you can borrow. If you improve it, you could save a lot of cash in the end. Your credit report records your financial activity, including any loans or credit card balances. These items will be reported by lenders to credit bureaus. It is possible to improve your credit score by looking over your report and paying particular attention to any errors.

Credit scores are based on a variety of factors, including whether or not you pay your bills on time and how much debt you owe. A good score means lenders are less likely to be risky, and this means better mortgage interest rates. Lenders will adjust rates to compensate for a low credit score.

FAQ

What should you consider when investing in real estate?

The first step is to make sure you have enough money to buy real estate. If you don’t have the money to invest in real estate, you can borrow money from a bank. It is important to avoid getting into debt as you may not be able pay the loan back if you default.

You should also know how much you are allowed to spend each month on investment properties. This amount must include all expenses associated with owning the property such as mortgage payments, insurance, maintenance, and taxes.

Also, make sure that you have a safe area to invest in property. It would be a good idea to live somewhere else while looking for properties.

How much money will I get for my home?

This varies greatly based on several factors, such as the condition of your home and the amount of time it has been on the market. Zillow.com shows that the average home sells for $203,000 in the US. This

Is it better for me to rent or buy?

Renting is typically cheaper than buying your home. It's important to remember that you will need to cover additional costs such as utilities, repairs, maintenance, and insurance. Buying a home has its advantages too. You will have greater control of your living arrangements.

What are the three most important things to consider when purchasing a house

The three most important factors when buying any type of home are location, price, and size. The location refers to the place you would like to live. Price refers the amount that you are willing and able to pay for the property. Size refers to how much space you need.

What are the cons of a fixed-rate mortgage

Fixed-rate loans tend to carry higher initial costs than adjustable-rate mortgages. Also, if you decide to sell your home before the end of the term, you may face a steep loss due to the difference between the sale price and the outstanding balance.

Should I rent or own a condo?

Renting could be a good choice if you intend to rent your condo for a shorter period. Renting can help you avoid monthly maintenance fees. However, purchasing a condo grants you ownership rights to the unit. You can use the space as you see fit.

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to Manage a Rent Property

While renting your home can make you extra money, there are many things that you should think about before making the decision. We'll help you understand what to look for when renting out your home.

If you're considering renting out your home, here's everything you need to know to start.

-

What do I need to consider first? You need to assess your finances before renting out your home. If you are in debt, such as mortgage or credit card payments, it may be difficult to pay another person to live in your home while on vacation. It is also important to review your budget. If you don't have enough money for your monthly expenses (rental, utilities, and insurance), it may be worth looking into your options. It might not be worth the effort.

-

What is the cost of renting my house? It is possible to charge a higher price for renting your house if you consider many factors. These factors include location, size, condition, features, season, and so forth. Remember that prices can vary depending on where your live so you shouldn't expect to receive the same rate anywhere. Rightmove shows that the median market price for renting one-bedroom flats in London is approximately PS1,400 per months. This would translate into a total of PS2,800 per calendar year if you rented your entire home. While this isn't bad, if only you wanted to rent out a small portion of your house, you could make much more.

-

Is it worth it. Doing something new always comes with risks, but if it brings in extra income, why wouldn't you try it? Be sure to fully understand what you are signing before you sign anything. Your home will be your own private sanctuary. However, renting your home means you won't have to spend as much time with your family. These are important issues to consider before you sign up.

-

What are the benefits? So now that you know how much it costs to rent out your home and you're confident that it's worth it, you'll need to think about the advantages. There are many reasons to rent your home. You can use it to pay off debt, buy a holiday, save for a rainy-day, or simply to have a break. You will likely find it more enjoyable than working every day. If you plan well, renting could become a full-time occupation.

-

How do I find tenants After you have made the decision to rent your property out, you need to market it properly. Listing your property online through websites like Rightmove or Zoopla is a good place to start. You will need to interview potential tenants once they contact you. This will help you assess their suitability and ensure they're financially stable enough to move into your home.

-

How can I make sure I'm covered? If you are worried about your home being empty, it is important to make sure you have adequate protection against fire, theft, and damage. You'll need to insure your home, which you can do either through your landlord or directly with an insurer. Your landlord will usually require you to add them as additional insured, which means they'll cover damages caused to your property when you're present. If you are not registered with UK insurers or if your landlord lives abroad, however, this does not apply. In this case, you'll need to register with an international insurer.

-

You might feel like you can't afford to spend all day looking for tenants, especially if you work outside the home. Your property should be advertised with professionalism. It is important to create a professional website and place ads online. It is also necessary to create a complete application form and give references. While some prefer to do all the work themselves, others hire professionals who can handle most of it. You'll need to be ready to answer questions during interviews.

-

What should I do once I've found my tenant? If you have a contract in place, you must inform your tenant of any changes. You may also negotiate terms such as length of stay and deposit. Keep in mind that you will still be responsible for paying utilities and other costs once your tenancy ends.

-

How do I collect rent? When the time comes to collect the rent, you'll need to check whether your tenant has paid up. You'll need remind them about their obligations if they have not. After sending them a final statement, you can deduct any outstanding rent payments. If you're struggling to get hold of your tenant, you can always call the police. The police won't ordinarily evict unless there's been breach of contract. If necessary, they may issue a warrant.

-

What can I do to avoid problems? Renting out your house can make you a lot of money, but it's also important to stay safe. Ensure you install smoke alarms and carbon monoxide detectors and consider installing security cameras. Make sure your neighbors have given you permission to leave your property unlocked overnight and that you have enough insurance. You should not allow strangers to enter your home, even if they claim they are moving in next door.