If you are in the market for a home equity line of credit, you can apply for a U.S. Bank HELOC to finance home improvements and debt consolidation projects. This type of line of credit is flexible and can save you on taxes and closing costs. With no application fees, you can get the money within three working days. Customers receive a 0.5 per cent discount on the interest rate. This makes this a great choice for all kinds of needs.

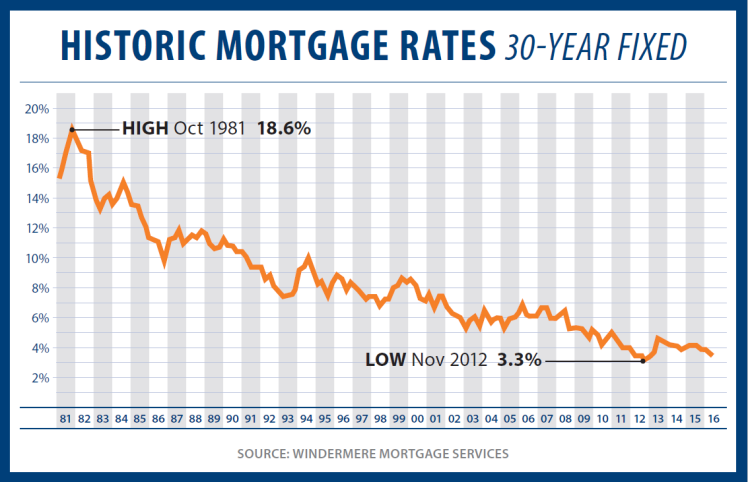

Rates

US Bank offers home equity credit (HELOC), services to borrowers across the country. The bank was established in Minneapolis, MN and offers services in all 50 US states as well as Washington DC. HELOCs, secured lines of credit, allow approved borrowers to get funds online, by credit card or check. The maximum amount of a loan depends on the creditworthiness, property value, and amount of the mortgage.

HELOCs typically have variable interest rates. But some lenders offer fixed interest options. Fixed interest options allow borrowers to make predictable monthly payments, and they don't fluctuate in line with federal interest rates. While fixed interest HELOCs can be more costly than variable HELOCs due to their higher cost, they are still a good option if interest rates are expected to rise.

Fees

The fees associated with HELOCs are important to know if you're thinking of taking out one. Inactivity fees can be charged by lenders to accounts with low activity. Transaction fees may be charged by other lenders for every use of your credit line. Some banks also charge fees for early repayment of HELOCs. These fees can reach up to $500 per payment and add up to $90 annually.

US Bank does not charge closing fees on its home equity products. However the bank charges for certain escrow related fees, such property insurance. A bank account has an annual fee. However, this can be waived for those who have the platinum checking package. While the annual fee does not apply to all states, it is an additional cost that you should be aware of. Additionally, the annual fee will apply if your HELOC is not paid within 30 days. You will be charged one per cent of the original amount up to a maximum $500.

Draw period

A HELOC's draw period is the time that you can borrow money for a particular purpose. HELOCs are available for a maximum of 10 years. The draw period allows you to repay the amount with either interest only or full repayments. A significant portion of the loan's cost is affected by the draw period for a HELOC. It is important that you know how much money you can afford before the draw period ends.

The draw period may be too short for you to withdraw the full amount. You can refinance your HELOC if you are concerned. This will ensure that you don't have to worry about a substantial increase in minimum payments. Refinance the entire HELOC amount following the draw period.

Minimum credit score required

One of the most important requirements for a HELOC is a high credit score. A high credit score is a guarantee to lenders that borrowers will be responsible and repay the money. It can also lead to lower interest rates. If your credit score is not high, you may not be able to take out this loan.

HELOCs have interest rates that are lower than other credit forms, but they are still subject to change due to the Wall Street Journal prime rate. It is possible that approval could take up until 45 days. Lenders need to approve the property's valuation.

FAQ

What are the pros and cons of a fixed-rate loan?

Fixed-rate mortgages lock you in to the same interest rate for the entire term of your loan. This will ensure that there are no rising interest rates. Fixed-rate loans offer lower payments due to the fact that they're locked for a fixed term.

How do you calculate your interest rate?

Market conditions impact the rates of interest. The average interest rate for the past week was 4.39%. Add the number of years that you plan to finance to get your interest rates. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

What are the three most important things to consider when purchasing a house

Location, price and size are the three most important aspects to consider when purchasing any type of home. The location refers to the place you would like to live. Price is the price you're willing pay for the property. Size is the amount of space you require.

What is reverse mortgage?

A reverse mortgage lets you borrow money directly from your home. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types to choose from: government-insured or conventional. Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers repayments.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to find an apartment?

Moving to a new place is only the beginning. This involves planning and research. This includes researching the neighborhood, reviewing reviews, and making phone call. You have many options. Some are more difficult than others. The following steps should be considered before renting an apartment.

-

It is possible to gather data offline and online when researching neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Online sources include local newspapers and real estate agents as well as landlords and friends.

-

Review the area where you would like to live. Yelp. TripAdvisor. Amazon.com all have detailed reviews on houses and apartments. You might also be able to read local newspaper articles or visit your local library.

-

Call the local residents to find out more about the area. Talk to those who have lived there. Ask them what they loved and disliked about the area. Ask for recommendations of good places to stay.

-

Check out the rent prices for the areas that interest you. Consider renting somewhere that is less expensive if food is your main concern. However, if you intend to spend a lot of money on entertainment then it might be worth considering living in a more costly location.

-

Learn more about the apartment community you are interested in. How big is the apartment complex? How much is it worth? Is it pet-friendly What amenities do they offer? Are you able to park in the vicinity? Do you have any special rules applicable to tenants?