Personal loans can be more advantageous than home equity loan when it comes to borrowing money for home improvements or debt consolidation. Home equity loans offer tax benefits and a shorter repayment term. It is possible to not have enough equity in your house if you are just starting out with home ownership. Equity is your home's total value less the amount you owe. This equity can take many years to build depending on how quickly you pay your mortgage off and how high your home's value increases.

Personal loans come with shorter repayment terms

Personal loans generally have repayment terms between 2 and 7 years. Some lenders will allow for longer terms. The repayment terms for personal loans are generally shorter, which in turn means that there is a lower interest rate over the life of the loan. Personal loans are more costly than home equity loans due to their higher interest rates. Personal loans may also have a lower minimum loan amount.

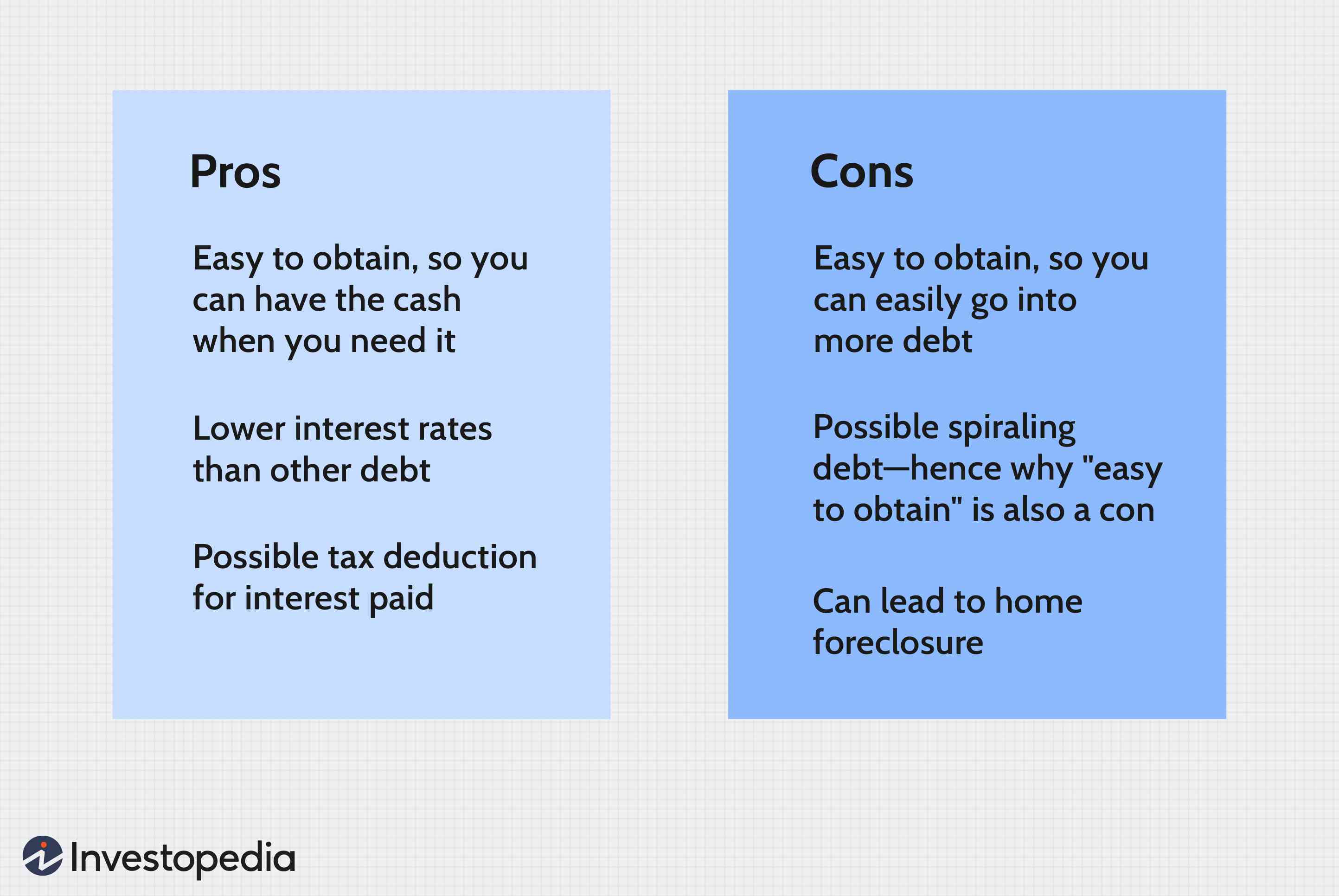

A personal loan usually requires less paperwork that a home equity loan. It should be easy for you to apply and qualify. However, if you have a poor credit score, you may be charged a higher interest rate than someone with excellent credit. This can put you in a riskier position and may even cause you to lose your home.

A personal loan has another advantage: it is flexible. A personal loan has a much shorter repayment period than a home equity mortgage. Personal loans can be used to pay off credit card debts or for home improvements. Lenders also look at your credit score and ability to pay back the loan. You should have good credit to be eligible for a personal loans.

Higher interest rates

Consider the interest rate before deciding between a loan for home equity and a personal loan. Personal loans generally have a lower interest rate than home equity loans, but their terms are often longer. Unlike a personal loan, a home equity loan is secured by the home and you can lose your home if you default on the payments.

Personal loans typically have a term of between two and seven years. However, some lenders may offer loans with longer terms. A home equity loan lasts for five to 30 year and is repayable with the proceeds of the sale.

The interest rate on a home equity loan is much lower than a personal loan, typically between 5% and 6%. While the interest rate of a home equity mortgage will fluctuate, it is still substantially lower than a personal or small-sized loan. Furthermore, a home loan's interest rate is tied to your credit rating and your income. A personal loan has a fixed interest.

Repayment terms that are longer

There are advantages and disadvantages to both personal loans and home equity loans when it comes borrowing money. Personal loans, on the other hand, do not require collateral and come with lower interest rates. However, they do require borrowers to have good credit. Personal loans can often be funded faster.

Personal loans are better options for those with a good credit history but lack the equity in their home. They can also be more costly and may have higher fees if you are late paying or your fault. In some cases, personal loans can create more debt than home equity loans, especially if used to pay off credit cards.

These loans are better for those who need larger sums of money. These loans often have lower interest rates than traditional loans and can be paid off more quickly. For those with substantial equity in their home, these loans might be more affordable. Both types are suitable for debt consolidation, emergency funds, and educational costs.

FAQ

Should I use a mortgage broker?

A mortgage broker may be able to help you get a lower rate. Brokers are able to work with multiple lenders and help you negotiate the best rate. Some brokers earn a commission from the lender. You should check out all the fees associated with a particular broker before signing up.

Can I afford a downpayment to buy a house?

Yes! Yes! There are many programs that make it possible for people with low incomes to buy a house. These programs include government-backed loans (FHA), VA loans, USDA loans, and conventional mortgages. More information is available on our website.

What should I be looking for in a mortgage agent?

A mortgage broker is someone who helps people who are not eligible for traditional loans. They work with a variety of lenders to find the best deal. Some brokers charge fees for this service. Others offer free services.

What are the most important aspects of buying a house?

The three most important factors when buying any type of home are location, price, and size. Location is the location you choose to live. Price refers to what you're willing to pay for the property. Size refers to the space that you need.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to find an apartment?

When you move to a city, finding an apartment is the first thing that you should do. This process requires research and planning. This involves researching neighborhoods, looking at reviews and calling people. Although there are many ways to do it, some are easier than others. Before renting an apartment, you should consider the following steps.

-

You can gather data offline as well as online to research your neighborhood. Online resources include Yelp. Zillow. Trulia. Realtor.com. Local newspapers, real estate agents and landlords are all offline sources.

-

Review the area where you would like to live. Yelp. TripAdvisor. Amazon.com have detailed reviews about houses and apartments. You can also find local newspapers and visit your local library.

-

Call the local residents to find out more about the area. Talk to those who have lived there. Ask them about what they liked or didn't like about the area. Also, ask if anyone has any recommendations for good places to live.

-

Check out the rent prices for the areas that interest you. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. However, if you intend to spend a lot of money on entertainment then it might be worth considering living in a more costly location.

-

Find out information about the apartment block you would like to move into. Is it large? What price is it? Is it pet-friendly? What amenities are there? Do you need parking, or can you park nearby? Are there any special rules that apply to tenants?